Money McBags promised he would get to JOEZ today and he finally had time to break down their terrible quarter where they once again managed to grow their top line faster than Heidi Montag grew her topline while shrinking their bottom line as if profits would give them whatever is worse than AIDS (and for the record, things worse than AIDS include front row tickets to a Robin Williams stand up show and mayonnaise). This company is just flat out unbelievable as their management team might be worse at their jobs than Jewel’s dentist and less shareholder friendly than MLNK’s management team (but at least with MLNK, there is an activist coming in, whereas what activist would want to but a trendy jeans company?).

{kind=link}

{kind=link}

—

How a company continues to grow top line 20% while becoming less profitable, yet still has shareholders, is something Money McBags understands less than he understands that Dancing With The Stars thing (though Money McBags would tune it in to Pole Dancing With The Stars, especially if one of the stars were Kate Bosworth and Money McBags were supplying the pole). So lets look a bit closer at the Q and see the positives and the negatives (and we’ll start with the negatives because we’re still pondering the positives):

{kind=link}

—

Negatives:

—

1. Growth continues to slow. They company grew top line 20%, which for a company selling a sort of high priced consumer product in this economy would usually be a good thing, but for JOEZ, we continue to see the second derivative of growth come down faster than a manic depressive after an eight ball. As Money McBags said when he broke down their last Q (and was equally as skeptical as he remains today), growth for this company over the past 4 years was 30%, 35%, 10%, and 16% and now they have had 4 consecutive quarters of no more than $25MM in revenue (the last 4Qs starting with Q4 2009 are $25.22MM, $23.18MM, $25.89MM, and now $25.53MM). So while y/y growth may still sort of look good off of the recessionary bounce (though praising ~20% growth off the recessionary bounce is like praising an author for being more linear than Thomas Pynchon or an economist for making more sense than Ben Stein), sequential growth was negative and in Q3 last year, sequential growth was ~24%. So calling this a growth company is getting to be a very tenuous description, as tenuous as calling Junior Seau a good driver.

—

2. And it’s not just overall growth that is slowing, but it is being driven by slower growth with their core customer and in their core segment. JOEZ wholesale business, which is ~85% of their business and has been their only business until their recent foray in to the retail world was up only 7%. Shit WMT grew almost 7% (well, 3% to be exact, but on the award winning When Genius Prevailed we round up to the nearest 7), and no one would call WMT a growth company.

—

But it’s not just that the core business is slowing, it’s that their womens business was up only 3% and that is ~80% of their wholesale business which proves that jeggings can only carry a business so far. Look, JOEZ is a company completely reliant on fashion trends and the fact that those trends have seemingly stopped resonating with women is a potentially bigger issue for this company than not wearing a condom was for John Edwards or not ducking was for John Lennon.

—

But the scariest part of all of this for JOEZ is that their denim business, and remember this company is called Joe’s JEANS, not Joe’s Tees, not Joe’s non-denim pants, and not Joe’s bottoms, was down 10% in the womens segment (if Money McBags correctly understood the transcript) and they are now relying on their non-denim business to help them grow out of the current sluggishness (and to be fair, their non-denim business is performing decently). And this is reason number 69 why Money McBags rarely buys a single product trend businesses (you hear that ZAGG?), because eventually they need to find the next fucking thing and go ask the guy who invented parachute pants what happened to him when the clock struck 1990.

—

Sure the non-denim segment could hit on the next big thing and push this company to new SKUs and products, but that is not something on which Money McBags would bet (though he would give JOEZ and the points for anyone who wants to gamble). It is hard as fuck to stay atop the fashion industry as trends tend to last shorter than Natalee Holloway in Aruba (and yes, Money McBags is going to hell for that one), so the first thing to look for in a company like this is sales slowing to women (especially to women in their CORE business). It’s simple, women are the shoppers and the trend setters because they need to own the hot item to be considered cool enough to date so they can finally get married and thus stop having to swallow. So having growth to that segment moderate is not good.

—

3. Gross margin was down from 49% to 46% y/y, though up from 44% sequentially. This is what happens when you have to discount like a 65 year old “sales girl” at the NSFW Bunny Ranch and you also move in to lower margin products (JOEZ’ non-denim growth). Those two things make more of a double whammy than finding the girl you brought home on a Saturday night not only had herpes, but also had a penis.

{kind=link}

—

On the call, management said that non-denim (which is a whopping ~16% of their business) should see margins go from 50ish % to 70ish % next year by moving their sourcing from China to India and Peru. Yeah, that’s right, a management team that fucked up the accounting on an earn out and has mastered unprofitable growth like bizzaro Warren Buffetts has discovered places cheaper to do business than China. Why the fuck is every other company moving production to China if dingdongs like JOEZ can find cheaper places to do business and juice up margins by ~30%? Money McBags buys that BS margin expansion story about as much as he buys Larry Craig’s wide stance story. It just makes no sense, but even if it is true, increased margins on ~15% of sales isn’t going to move the needle.

—

4. Retail margins also tanked. Joe’s basically got stuck with a bunch of inventory they couldn’t move in their great new retail stores so had to discount the fuck out of them sending margins down from 66% to 55%. They said margins are back up to that 66% range but that is until a month from now when they are once again trying to clear shelf space for new inventories and their stuff hasn’t moved. So while it was great that retail sales were up 223% to $4.2MM, they were at reduced margins and the retail segment still lost money.

—

5. Operating expenses continue to increase. This quarter they were up ~600k sequentially and remember two quarters ago when they called part of the step function jump up a result of one-timers? Well those one-timers have now become a full on friend with benefits except the only benefits shareholders are getting is a lower stock price.

—

6. Cash was down again, but it’s not like they need cash to open new stores, right? Oh what’s that? They do? Well shit, this company’s balance sheet reeks of equity raise so much that KITD’s CEO Kaleil Tuzman is getting a stiffy. They have now blown through ~$6MM in cash this year, were down ~$2MM this Q, and have only ~$6MM left on the balance sheet.

—

On the call, management was asked point blank about generating positive cash flow and they gave some answer about inventory ramping down being the most positive driver of helping their cash but they seemed to pussyfoot around a straight answer to this and trust Money McBags, a foot is no place to put a pussy.

—

They said new store openings are ~$200k a piece, so perhaps they can keep afloat without raising more cash, especially when their new stores are slated for places like Dawsonville, Georgia where rent probably involves a used pair of dentures and some bed sheets (and note to brand strategists: If you’re trying to sell a trendy aspirational brand, don’t build a fucking store in East Asscrack, Georgia or Blue Ball, Pennsylvania. You want people to think they are getting something special, not something Ellie Mae Clampett would wear to a hoe down). So perhaps the $6MM cash on the balance sheet can tide them over, unless of course they have another 9 months like they just had where they burn through ~$2MM a Q.

{kind=link}

—-

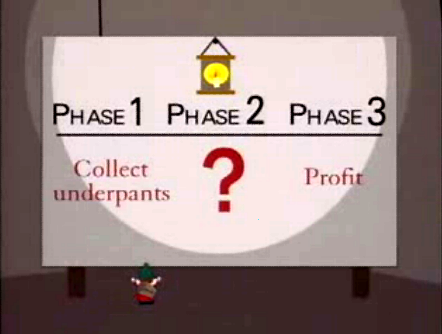

7. Profits were cut in half, despite revenue growth. Even taking out the doubling of the tax rate to 60 fucking % (which is such a high tax rate that it would turn even Joseph Stalin in to a Teabagger) as a result of their original merger deal which benefited shareholders about as much as having two Nobel prize winners on their board benefited Long Term Capital Management, they still destroyed incremental value from an operating perspective. Last year, on ~$21MM of revenue, they earned ~$2.8MM before taxes and this year, on ~$25MM of revenue, they earned ~$1.4MM before taxes. So on that extra $4MM of revenue, they managed to put up -35% margins which is a neat trick, though not as neat as find the button or the hidden ball trick. Their gross margins shrunk and their operating costs rose by 3MM and they basically had to discount to get inventory off the shelves. This management team is kind of like the mentally challenged underpants gnomes: Step 1: Sell Jeans. Step 3: Don’t profit.

{kind=link}

{kind=link}

—

Positives:

—

1. No one got hurt while putting up this quarter (unless you count shareholders).

—

2. Their non-denim business does seem to be catching on (though at reduced margins).

—

3. Money McBags just found a lovely young lady named Sasha Jackson, which has nothing to do with JOEZ, but you’ll all agree it is a very positive find.

{kind=link}

—

Conclusion: So what the fuck do we do with a company that just earned $.01 per share (down from $.03 per share) and continues their trend of unprofitable growth? Well we certainly don’t want to own it, in fact Money McBags would rather own the rights to WaterWorld II than JOEZ, but what is a fair value (other than maybe $0)?

—

With revenue basically flat for the last 4 Qs, we could just build off the $25MM revenue run rate and say their assawful performance this Q will continue and then put the company at a $.04 annual eps run rate and thus value them at ~10x that or $.40 but that would be too easy and very portfolio manager of us. Let’s say they can somehow grow 20% next Q to $30MM so end the year with ~$105MM revenue which would be 30% growth for the year (a number they haven’t hit since 2007, but whatever). Then maybe they can get 20% growth next year, but Money McBags is going to keep their margins at 45% because fuck if he trusts this management team to move inventory and stay on top of trends (which is as much luck as anything). If we grow operating costs by 10% to ~$46MM and tax them at 45% (thanks for the earn out guys), we get to ~$.09 per share for next year and that is as positive of an outlook as Money McBags can have for this company.

—

So what would you pay for $.09 of earnings for a company that is sort of growing but not really and whose management team has no idea how to profitably run a business? Would you pay 10x that? 15x that? Shit, Money McBags wouldn’t buy in for anything above $.90 so it’s not a terrible short right here. The problem is, they just need one good quarter where things fall in to place to give the semblance of being a real business which would kill your short since this stock is so volatile. That said, Money McBags doesn’t expect any big Qs soon, so while it is difficult to short a stock trading under $2, you can probably get a decent return here.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a Reply